Like any business document, a financial report is built to tell a story. Creative accounting, and something as simple as the ordering of information, means public gaming firms tell the story they want – with the headlines they want emphasized. But whatever order financial statements are written in, the facts and figures remain publicly available. All key performance indicators are documented and investors have to assess for themselves how a gaming company has actually performed, rather than how it wants to be perceived to have performed.

When making this assessment, however, a number of overlapping measures exist – and it can be difficult to ascertain which of them is most valuable. Revenue, profit (operating and net), operating cash flow and earnings per share are all relevant indicators that stand out on income statements. Where, though, does EBITDA fall within this list? While it typically sits second or third in a gaming financial report, especially among US organizations, how important is it in practice?

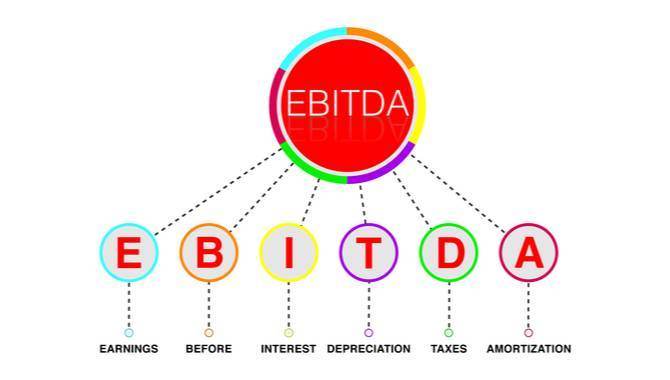

Representing earnings before interest, depreciation and amortization, EBITDA can be thought of as income generated purely from the selling of a company’s products and services. As Jason Ader, CEO of SpringOwl Asset Management, tells Gaming America, it’s the “closest and simplest measure” of establishing how much cash flow is generated by a business. After all, the significance of cash flow cannot be underplayed – a fact particularly emphasized during the current coronavirus pandemic. By comparison, earnings and earnings per share are affected by various external factors. As Ader says, “analysts and investors look at EBITDA because it most closely approximates the business cash flow, which is critical in assessing a business’s value.”

EBITDA and EBITDA margins, which show the percentage of a business’s total income generated through EBITDA, vary widely across the gaming industry, and some firms may present data on EBITDAR (the R standing for restructuring or rent costs) and others on EBITA or EBIT. While revenue is usually the first figure to be presented, taking all the credit so to speak, EBITDA can help investors read between the lines. This spring, for example, a number of trading updates from companies such as GVC Holdings, Playtech, William Hill and Flutter Entertainment spoke of projected EBITDA hits due to the absence of major sport and, consequently, sports wagering revenue.

Speaking to Gaming America in March, meanwhile, GVC CEO Kenny Alexander also provided an interesting case study. Indeed, Alexander projected there would likely be an EBITDA hit for GVC-owned Bwin when sports betting is regulated in the German market. But conversely, he asserted that the operator’s share price will rise as investors respond positively to a fall in EBITDA – in return for regulatory clarity in the German sports betting sector.

One benefit of EBITDA as a KPI lies in its lack of reliance on outside financial factors. As Ader explains, interest is a function of debt and interest rates, while depreciation and amortization are affected by several aspects of accounting methodologies. These can all “distort earnings.” However, the investor warns against viewing EBITDA as a lone “magic metric.” He says: “I think there’s no one measure; it’s very common to look at EBITDA because it gives you a sense of how much cash flow is coming out of the business before items that could negatively impact earnings per share; but it all matters.

“Revenue matters, too, in the context of how much revenue per employee, how much revenue relative to expenses and how much it costs to generate revenue; every company is different. So there’s no one magic metric to look at this, just like there’s no one metric in sports to tell you how good an athlete is. It all matters in the context of who the company is being compared against and what specifically you’re looking for in the company.”

The SpringOwl Asset Management CEO suggests earnings and earnings per share still hold value, too, for instance showing if a company has an inordinate amount of interest, or demonstrates a large scale of depreciation. High depreciation levels could suggest a gaming firm may have overpaid for acquisitions in the past or made investments in capital that’s falling in value. That depreciation affects the business’ earnings, and accountants do their best to match depreciation of assets and amortization of trademarks in line with the value the company loses every year. “Buildings depreciate, with the paint and the plumbing and all that stuff,” Ader adds, “and that’s why you have capital improvements.”

Another financial figure within the gaming industry, Sportech CFO Tom Hearne, places even less emphasis on EBITDA. Indeed, he believes “smart” investors can gain far more from evaluating a company’s operating cash flow. Initially asked how EBITDA compares to revenue as an indicator, Hearne says: “I think the question does make sense and, particularly with some of the changes in the accounting rules over the last year, I think EBITDA is becoming a less and less important measure. We have expanded to include significant KPIs like operational cash flow. At the end of the day, businesses talk about EBITDA a lot but the smart investors always look at cash flow.”

Hearne’s assessment is rooted in the value of understanding exactly how a firm’s revenue relates to cash. For Sportech, a retail and digital supplier specializing in sports betting and US horseracing, that is one of the key drivers in digitalizing its business. Moving a greater share of the organization online helps customers build better margins, according to Hearne, and reduces capital costs significantly. This, in turn, increases operating cash flow. “Those are the KPIs we focus on as we grow our business and I think they will become as important – or more important – than EBITDA,” adds Hearne.

Despite pointing out that there’s no “big difference” between the two measures, when this is put to Ader, he agrees operating cash flow is perhaps the superior KPI. “It’s usually net income and then you add back your non-cash charges,” he says. “Then you’re adjusting for any changes in working capital, which could be changes in inventory levels and methods you go about securing funding for your business. So that gets down to exactly what I was saying: one would look at EBITDA to get a sense for the cash generated out of the business. But I would agree that an even better measure is operating cash flow, which gives you a truer measure of the cash being generated by the regular activities of the business over the period you’re looking at.”

EBITDA’s primary use is for business valuations, according to Ader, gauging where gaming companies across the public sector trade market value, plus debt, divided by EBITDA. That formula remains important for valuations and investors will continue to look at it. Investors, though, are equally encouraged not to look solely at EBITDA before making any final decisions, although it remains one of the more useful measures on an income statement. Ultimately, EBITDA serves a worthy purpose in providing a more honest, undistorted picture of a gaming company’s earnings, although it’s worth noting the argument for operating cash flow as an even more effective indicator.